What assets should you put in your trust? Avoiding probate, planning in case of incapacity, and making things as easier for loved ones after your death are all things to consider. Hawaii estate planning attorney John Roth goes what assets should generally be kept in trust and why.

A trust AS PART OF AN ESTATE PLAN

First of all, estate planning is the proactive process of setting up a plan in case of your incapacity or death. The estate planning documents include a will, advance health-care directive, power of attorney, and sometimes a trust. These documents, drafted by an attorney, help someone step into your shoes to make decisions on your behalf, during your lifetime and after your death. After your lifetime, these documents control who inherits your property and how and when that inheritance is received. Including a trust in your plan may clairify how you want your estate handled and help to minimize administration costs and unnecessary taxes.

WHAT Assets should be in my trust?

Setting up a trust is the first step, which involves meeting with an attorney and drafting the trust document, then signing it with a notary. The second step is to fund your trust, by naming assets to the trust. What assets should you put in your trust?

If you have a revocable trust as part of your estate plan, Congratulations! You've accomplished the first step of creating an estate plan, but there is another step which includes funding your trust. Funding a trust is to transfer certain assets into your trust. Think of a trust like a business entity or protective container.

Some people don't transfer any assets into their trust, and when they die, their will pours remaining assets into the trust. So, when you have a trust, you always also have a will that makes sure the assets, that for whatever reason are not in your trust and don't have designated beneficiaries, when you die, get transferred into your trust. Then your trust can control who the beneficiaries of those assets eventually are and how they are managed. However, there are certain things that you can accomplish by transferring assets into your trust during your lifetime.

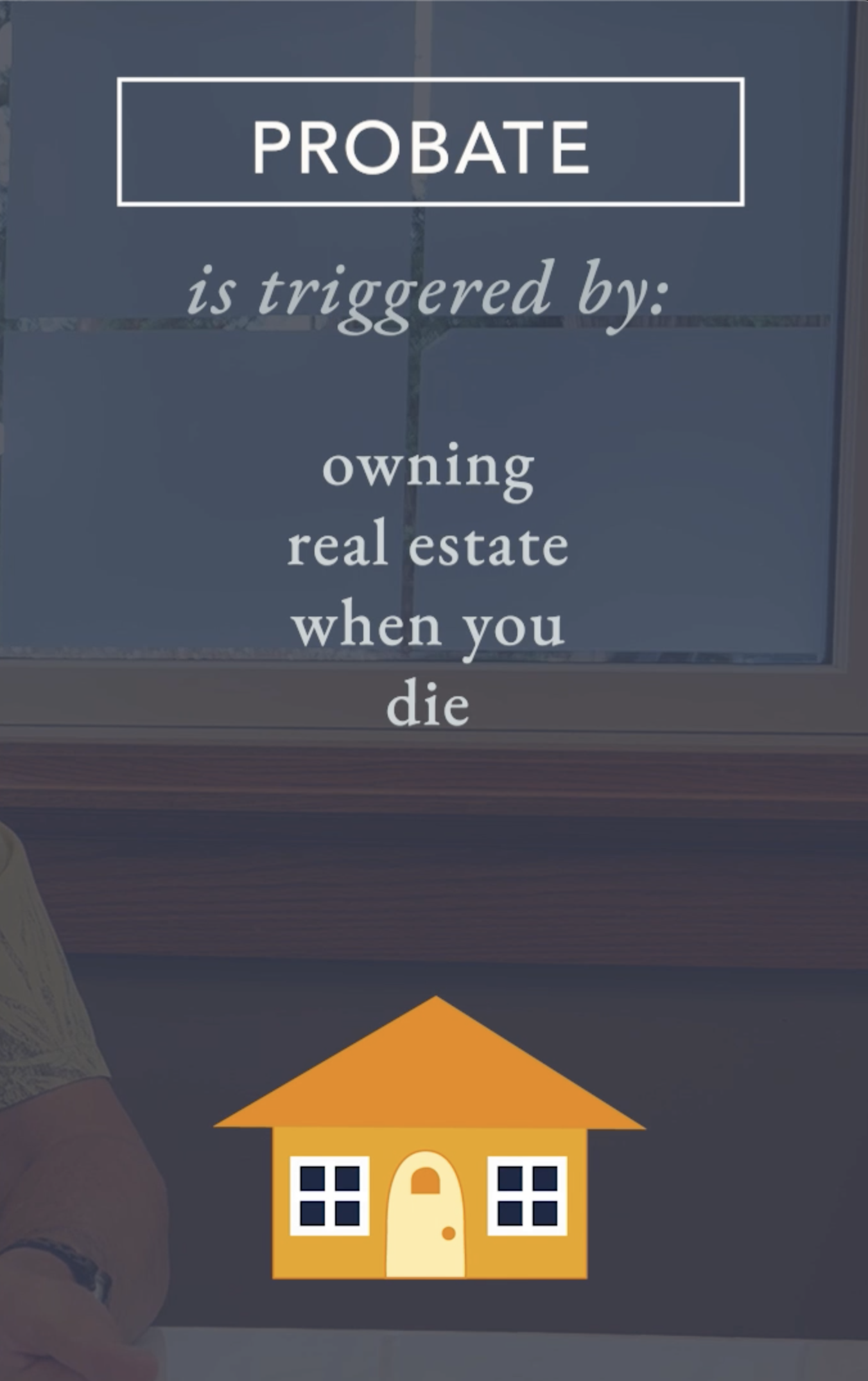

Probate avoidance

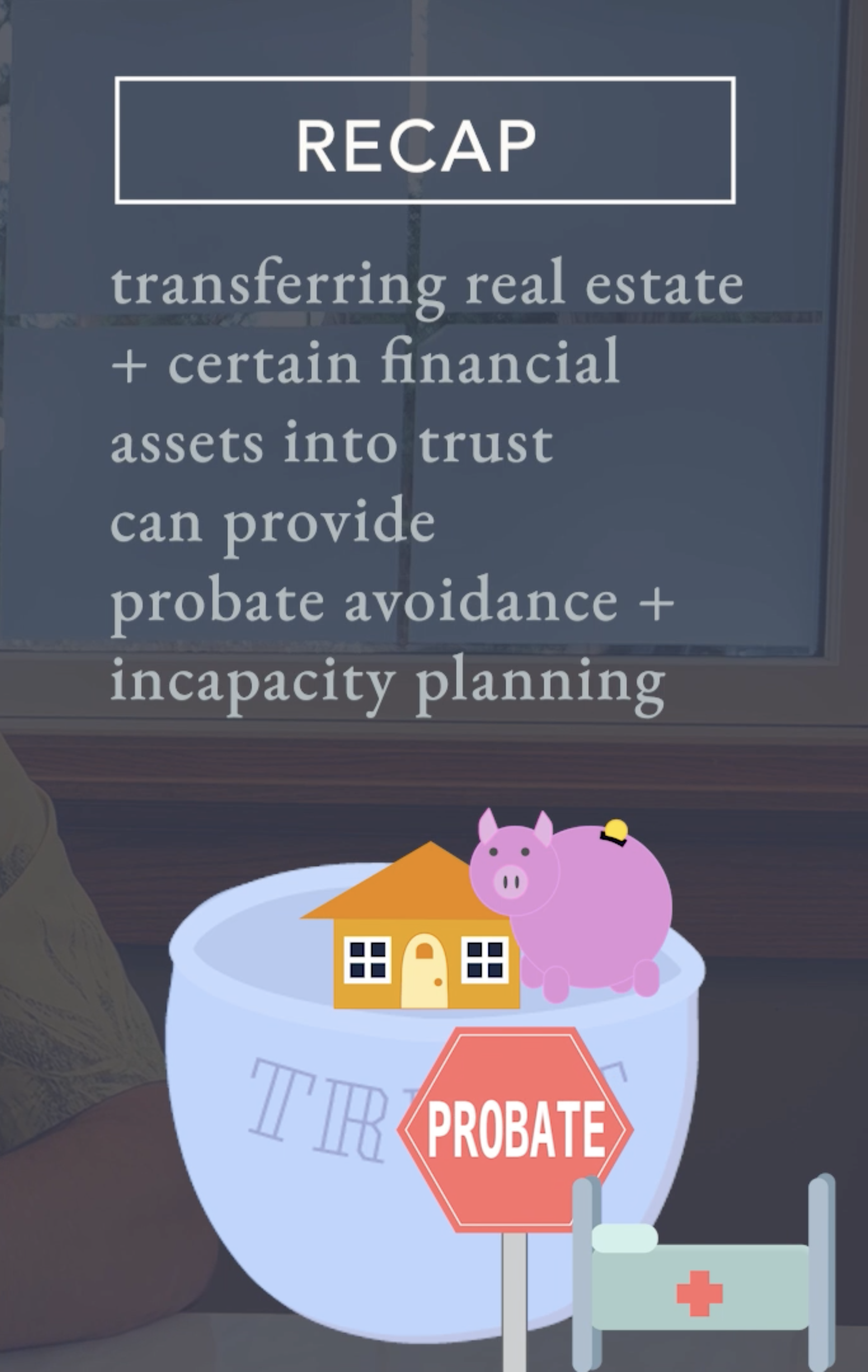

Transferring assets into your trust during your lifetime can accomplish probate avoidance and incapacity planning. Letʻs discuss probate first. Probate is triggered when someone dies owning certain assets, which include real estate. If probate avoidance is one of your goals, transferring your real estate into your trust will accomplish avoiding those assets from triggering probate.

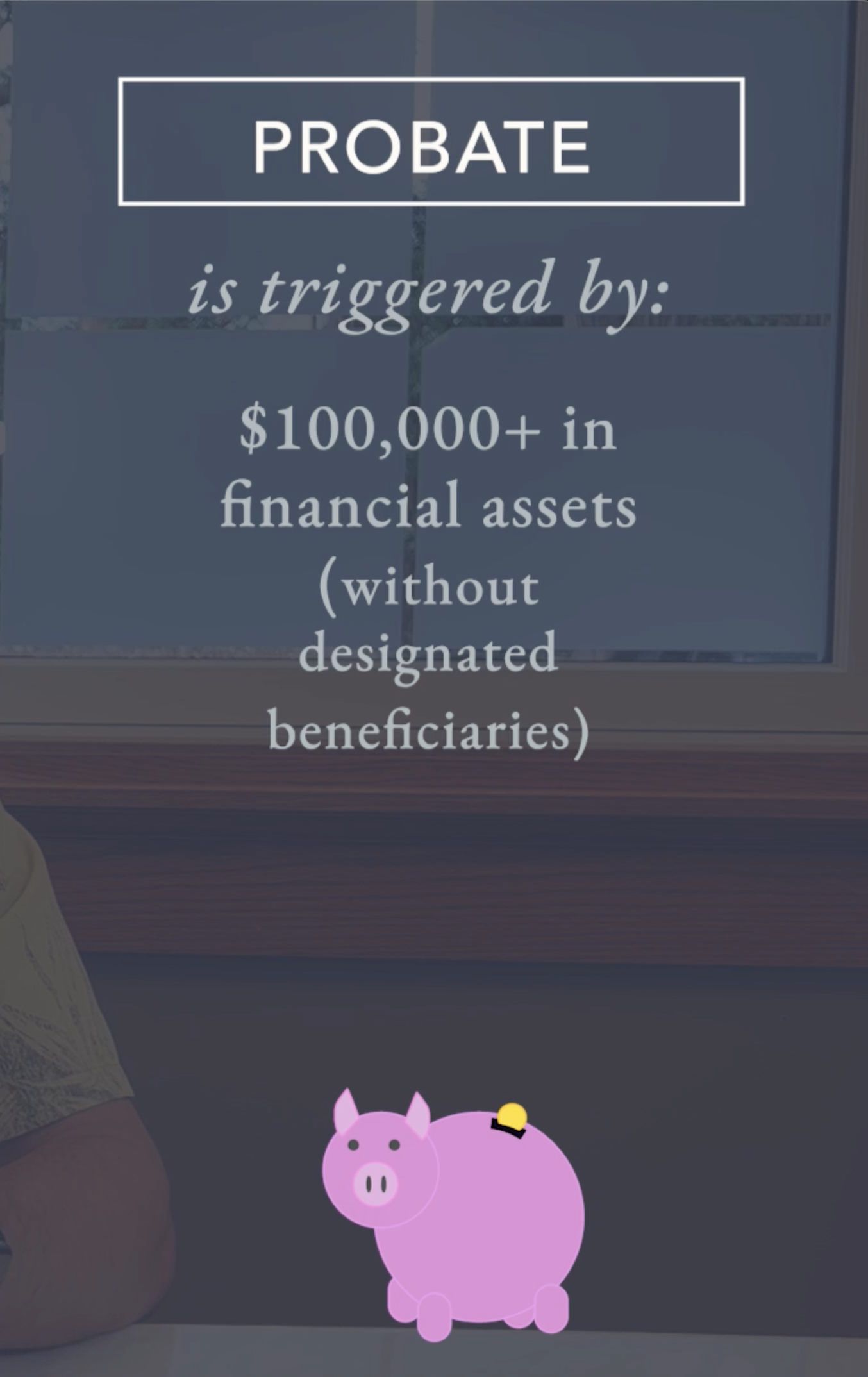

Also, other financial assets, that do not have designated beneficiaries that total $100,000 or more, also trigger probate. Generally, your larger savings, brokerage, and investment accounts should also be held in your trust. Some people prefer to use designated beneficiary provisions to avoid probate for those larger investment savings type accounts.

Incapacity planning

Yes, designating a beneficiary on an account does bypass probate, but it does not provide for the incapacity planning that is accomplished by transferring those larger accounts into your trust. For example, during your lifetime, if you're living, but you're having a hard time managing your own affairs, such as writing checks and paying bills, you can step down and you can resign as the trustee of your own trust. Someone you appoint and trust steps in to handle the finances. Or, if you don't have the foresight, opportunity, or desire, you can be removed as trustee of your trust. Generally, we define in our documents that if two physicians agree that you lack the capacity required to manage your own affairs, you can be removed. Then your successor trustee, maybe one of your children, can step in and become the trustee of your trust, while you are still alive, and make sure that you are taken care of, bills are paid, and your assets are managed for your benefit during your lifetime.

So basically, when you transfer an asset into your trust, whether it's your real estate or investment, savings, or brokerage type of accounts, you benefit from potential probate avoidance and incapacity planning. Anything in your trust while you're alive, managing your own affairs is treated as yours. You are the trust. You're the trustee. You're the beneficiary. The trust uses your Social Security number. However, when something is held in your trust during your lifetime, generally, it makes it easier to manage in the event of your incapacity or death. Of course, every situation is different, and your goals and specific assets may require a unique plan.

What happens if I don’t have a will OR TRUST?

If you die without a plan in place your property passes instead in accordance with the state law in which you lived. Think of these laws as a standardized back-up will written by the state legislature on behalf of anyone who dies intestate, that is, without a will.

Despite the legislature’s good intentions, property controlled by intestate rules sometimes passes to people the decedent wouldn’t have selected. For example, any such property passing to the decedent’s children will be shared by them equally, even if the decedent had made clear (but not in a valid will) that she did not want a particular child to get anything … and even if that child had once talked the parent into giving that child “his inheritance” before the parent died. That child would probably end up with a double share.

We hope you found this information on funding your trust in Hawaii helpful. If you have any questions please comment below or contact us.

RELATED TOPICS:

JOHN ROTH

John is the founder of Hawaii Trust & Estate Counsel, a statewide Hawaii estate planning law firm with offices in Waimea, Hilo, Kona, Maui, and Honolulu. He has taught Estate Planning at the Richardson School of Law, and business law courses at the University of Hawaii—Hilo. He started “Just Ask John” as a monthly newspaper column answering commonly asked estate planning questions, in the North Hawaii News, then in The West Hawaii Today. Now it’s an online blog and video series. ....MORE

MAKE AN INFORMED DECISION

Everyone has a different story and should have a unique estate plan. In most cases, the first meeting with one of our attorneys is complementary and serves the purpose of understanding your goals and educating you on your options. Depending on the option that is right for you, we will give you a price quote at the first meeting, before moving forward with your plan. Feel free to explore the basic information on our website.

This blog does not contain legal advice. You should not rely on this to determine what is in your own best interest. For legal advice, specific to your situation, you must meet with an attorney. All posts are based on hypothetical scenarios, not the actual circumstances of real clients.

LATEST VIDEOS

What assets should you put in your trust? Avoiding probate, planning in case of incapacity, and making things as easier for loved ones after your death are all things to consider.